I wrote recently of The Debt Fallacy – the widely held belief that the financial crisis was caused by government debt. If you read it you’ll recall that it’s fairly easy to prove this as a fallacy because figures for government debt are easily available. Nevertheless it’s a myth that is widely believed because the government puts a lot of effort into propagating it in the knowledge that most people won’t actually check.

Another fallacy that the government often uses hand in hand with this is one regarding interest rates. It goes something like this:

Interest rates on UK debt are low because the markets have built confidence in the UK’s economy because of the austerity measures. If the government were to increase public spending, the markets would lose this confidence resulting in the UK losing its AAA credit rating and interest rates on our debt soaring.

This, ladies and gentlemen, is the Interest Rate Fallacy – the widely held belief that interest rates are low because of the market’s confidence in our economy. To show why this is a fallacy is a little harder than it was with The Debt Fallacy because I can’t just download a graph from the IMF website. So before reading on you might want to get a cup of tea and an exciting type of biscuit, such as a Jammy Dodger.

All settled? Then let’s get started. Before we tackle the fallacy we need to look briefly at what government debt is and why people buy it at all.

How does the government borrow money?

The government borrows money by issuing bonds. A bond is essentially an IOU, which anyone can buy. It will say something like, “I will borrow £100 from you for 10 years and at the end of the 10 years I’ll pay you back your £100. As compensation for you not having access to your cash for 10 years, I will additionally pay you interest at an annual rate of 5% for those ten years.”

Why does someone lend money to the government?

Imagine that I have £100 in cash. I could keep the £100 as cash or use it to buy a bond. Cash is good because I can do useful things with it like buy stuff. However, I need to think about my future and if I want to save money for later rather than spend it now then I would be better off buying a bond because I get paid interest as compensation for me not having access to my money. If I want to spend now then cash is good. If I want to save now then bonds are good.

What determines the interest rate on my bond?

The interest rate on a bond is determined by the rate that savers are willing to accept in compensation for not having access to their cash for the period of the bond. So if I want to invest my £100 for 10 years what are the factors that will influence the rate I am prepared to accept?

Probability of default

If I tie up my money with someone for 10 years then it’s quite important to me that they don’t go bust during that time because if they do I will lose my money. If I am lending to someone risky I might decide to ask for a higher rate of interest in order to compensate me for the risk that they might not be able to repay me.

Demand for bonds vs Demand for cash

If I want to save money and everyone else wants to spend money then I can probably get a high rate on my investment. If there are few savers and lots of spenders in the market (i.e. the demand for bonds is low and the demand for cash is high) then the government will need to offer better rates to attract investors. Conversely if there are lots of people who want to save money and few who want to spend, the government can offer much lower rates knowing that there are still lots of people who will invest anyway.

Expected future short-term interest rates

That’s a mouth full isn’t it?

Short-term rates are set (in the UK) by the Bank of England. These rates determine the rate I can get for investing money for a short period of time.

If I am going to invest for a longer period of time, my expectation of what the Bank of England will do with short-term rates in the future is important. This is all sounding a bit wonkish so I’m going to explain with an example. Imagine the following scenario:

- I live in a country where the government offers two different types of bond

- One lasts for one year

- The other lasts for 10 years

- I have £100 that I would like to invest for ten years

I have a choice:

- Invest my money once in the 10 year bond

- Invest my money ten times (once every year) in one year bonds

If I choose the first option then my money is tied up for ten years at the pre-agreed rate of interest. If I choose the second option then every year when I invest my money again I get whatever the new short-term rate set by the government is. Supposing that short-term rates are 2% but I expect them to rise by 0.25% every year. My expectation of what the second option looks like is this:

| Year |

Interest Rate |

Value of Savings |

| 1 |

2.00% |

£102.00 |

| 2 |

2.25% |

£104.30 |

| 3 |

2.50% |

£106.90 |

| 4 |

2.75% |

£109.84 |

| 5 |

3.00% |

£113.14 |

| 6 |

3.25% |

£116.81 |

| 7 |

3.50% |

£120.90 |

| 8 |

3.75% |

£125.44 |

| 9 |

4.00% |

£130.45 |

| 10 |

4.25% |

£136.00 |

Therefore for me to decide that investing in a 10 year bond is worth it, I need a rate of at least 3.1225%, otherwise I expect to lose money on it.

Conversely, if I expect interest rates to go down then I will be happy with a lower rate for my 10 year investment.

Still with me? Good. Get yourself another Jammy Dodger – you’ve earned it.

Why are interest rates low now?

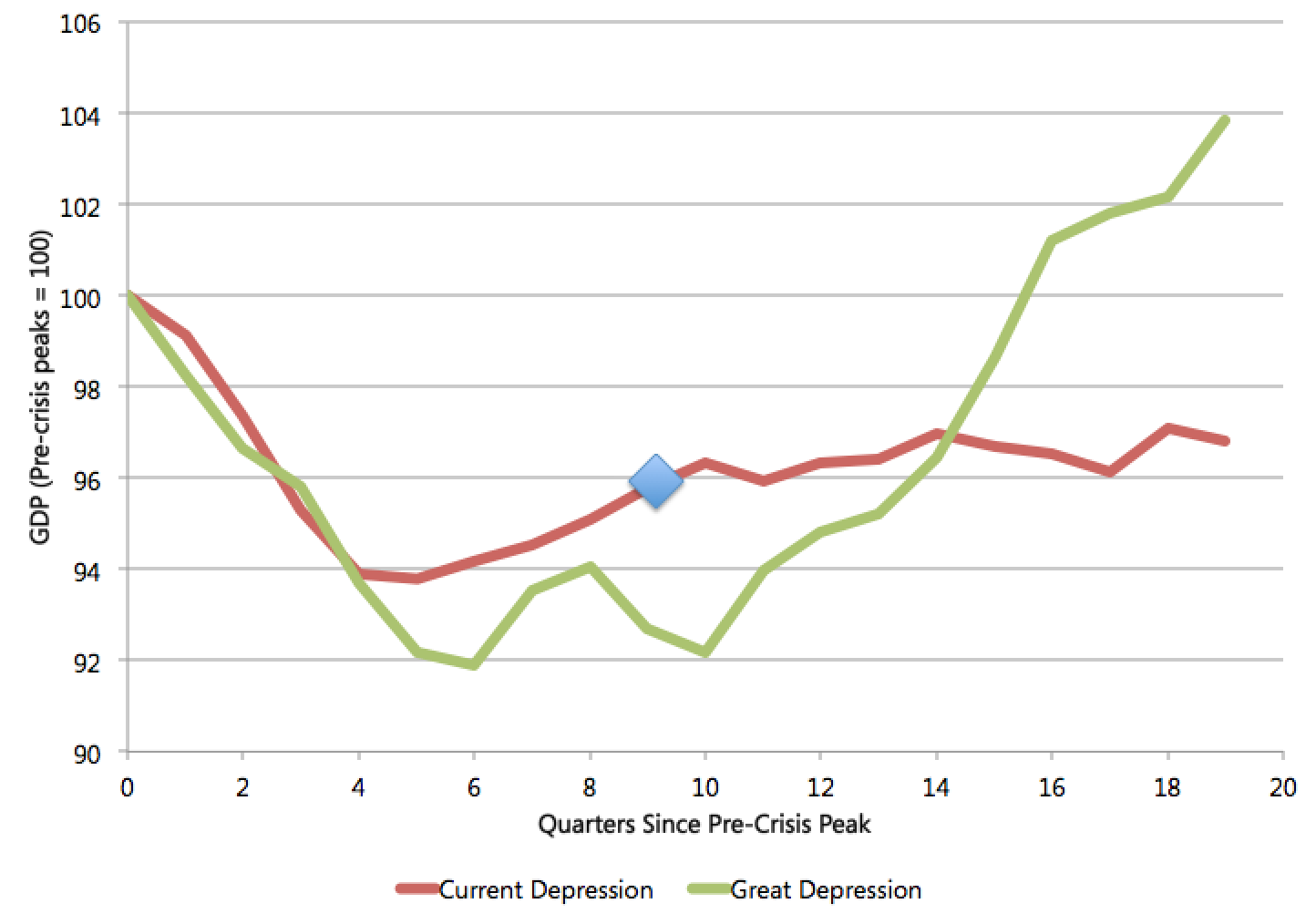

The government says that interest rates are low because the markets have lots of confidence in our economy because of their austerity policy. Lots of people lap this up as gospel but let’s stop for a moment and think about that. The government is borrowing at the lowest rates in the country’s history at the same time that the economy is in the longest depression in living memory. Would this really be the point in history that confidence in our economy hit an all time high?

Umm… no. So using what we’ve learnt, let’s look at some sensible explanations instead.

Expected future short-term interest rates

Short-term interest rates are very low at the moment. We know why – in reaction to the financial crisis, the Bank of England cut interest rates in an attempt to boost the economy. (They cut them to 0.5% in March 2009 where they have remained ever since.)

Remember though, that long-term interest rates are determined by what the market expects short-term rates to be in the coming years. One explanation (this is the right one by the way so pay attention) for low long-term interest rates would be that the markets expect The Bank of England to keep short-term interest rates low for the foreseeable future.

Why would the markets expect The Bank of England to keep short-term rates low in the future? Well remember why short-term rates became low in the first place – an attempt to stimulate a weak economy. If the market expects the UK economy to remain depressed in the future they will expect The Bank of England to keep short-term rates low. If they expect a recovery is just around the corner they will expect short-term interest rates to rise and they will demand higher long-term rates in compensation.

Demand for bonds vs Demand for cash

Ok, I said the last one was the right answer but it’s important to consider this point too. The demand for bonds is huge at the moment. Why? Because when the financial crisis struck, people who had spent happily during the good years changed their behaviour dramatically and started saving. We are living in a world of people saving money rather than spending it. Again they are doing that because of a lack of confidence in the economy.

Probability of default

Enough of sensible explanations. Let’s look at a daft one. You’ll recall that people demand higher interest rates if they think that the person to whom they are lending might go bust before their bond matures. Therefore if the markets think that there is a good chance that the UK might go bust within the next 10 years they will demand higher rates for their 10 year bonds.

Let me be absolutely explicit here. There is absolutely no chance of the UK going bust in the next ten years. Despite the least economically competent government that anyone can remember, it is still impossible.

The UK is a large, developed economy whose debt is in a currency that they control. We print our own money – we can’t run out of it. Barring alien invasion, the UK will service its debt next year, the year after, the year after that etc. etc.

What about Greece?

A common comparison, used by George Osborne amongst others, is that Greece has a weak economy that is expected to remain weak but has high interest rates on government debt. They do but there is a difference between Greece and the UK and although George Osborne chooses to ignore it, it is a very big difference. When a country adopts the Euro they give up something very important – control over their currency. The countries that have seen their interest rates rise, Greece, Ireland, Italy, Spain, Portugal all have something in common – their debt is in a currency they can’t control.

But what about Argentina in 1999/2000?

Their debt was in US dollars so the same thing applies. They borrowed in a currency they could not control.

What about Iceland? They weren’t in the Euro and their government debt wasn’t that bad.

That’s true but Iceland’s three major banks had somehow been allowed to build up about €50bn of foreign debt between them. To put that into perspective, that was about 600% (!) of Icelandic GDP. Nice one Icelandic banking dudes.

What if the UK loses its AAA credit rating? Interest rates will soar!

The first thing to mention is that this argument assumes that austerity will prevent any downgrade of the UK’s credit rating. I’ll return to that point though because I want to tell you a few things about credit rating agencies first.

A credit rating agency is a private company that expresses an opinion about a borrower’s likelihood of repaying money they have borrowed from someone else. You will note that the UK currently has a AAA credit rating, which is the highest possible. (Not all agencies use AAA as a code to signify the safest borrower but the UK has the highest rating from all of the major ones.)

For example, the biggest credit ratings agency, Standard & Poors, gives the UK a AAA rating. To understand what that rating means, let’s benchmark it against something else to which Standard & Poors have given a AAA rating.

In the run up to the financial crisis, banks lent money to risky borrowers in the form of subprime mortgages. Those banks would then package up a few thousand of these dodgy mortgages together and sell them on to someone else. Guess what rating Standard & Poors gave to these packages of toxic debt? Yep, AAA!

Reread that last paragraph – the largest credit rating agency in the world gave their highest possible rating to packages of subprime mortgages. I am not a credit rating agency and you are not a credit rating agency but if you and I were forced to form an opinion on the creditworthiness of 2,000 subprime mortgages all mixed together we would probably not come to the conclusion that it was the safest investment possible. The credit ratings agencies did.

If you think I am cherry picking one (albeit hugely damning) example, I’ll give you another. On the 15th September 2008, Lehman Brothers went spectacularly bankrupt. All three of the major agencies rated Lehman Brothers as a low risk counterparty.

So the upshot of this all is that no one actually listens to these people. S&P downgraded the United States from AAA to AA+ last year. Did the markets all panic and think that the US was about to go bust? No. They ignored the discredited opinion of an organisation who thought that subprime mortgages were a good investment and went their about business as usual. Interest rates on US bonds actually went down.

But wouldn’t rates go up if we abandoned austerity?

The last refuge of the “Austerity=Low Interest Rates” cult is always, “Even if your ‘economics’ mumbo-jumbo is right about the reasons for low rates, if we actually took advantage of them and borrowed some more money, those rates would not stay low for long!” I’ll address that now.

Demand for bonds vs Demand for cash

As I’ve mentioned before we are currently in a liquidity trap. In normal times, cutting short-term interest rates stimulates spending. A liquidity trap occurs when we have already cut interest rates as far as they can go but people still want to save. At the moment, no one wants to spend money but The Bank of England have already cut rates to almost zero.

Being in a liquidity trap means that we would need a significant change in behaviour back from saving to spending before it made any difference at all to actual interest rates. The interest rate we would need to get people spending is negative but The Bank of England can’t set a negative rate* so we’re left with demand for bonds far outstripping demand for cash. Being in a liquidity trap isn’t good news but it does at least mean we can increase borrowing without changing the interest rate.

Probability of default

What would happen if the markets thought the UK was about to go bust and everyone tried to sell their bonds all at once? (Yes, I know the idea of the UK going bust is stupid but people use this argument a lot so I should address it.) Unlike Greece, Ireland, Spain, etc we have a flexible exchange rate. If the markets suddenly decided to start offloading UK government debt interest rates would not actually rise. What would happen is that the pound would just devalue** and interest rates would stay the same.***

Summary

So as we’ve seen interest rates are low because everyone wants to save rather than spend and the markets expect short term interest rates to be low for the foreseeable future because they expect the economy to remain weak.

We’ve also seen that credit ratings agencies’ opinions are not worth listening to. Despite the government claims that austerity is the barrier against a downgrade, I fully expect the UK to be downgraded next year. And you know what? If that happens the markets won’t give a toss and long term interest rates will remain low.

If you have read this whole post down to here then well done – treat yourself to another Jammy Dodger. You know now what determines interest rates on government bonds and you know that it has the opposite to do with everyone being happy about our economy. The sad reason for low interest rates is simply that the markets expect our economy to remain bad for a long time yet.

And to be honest, who could really blame them?

RedEaredRabbit

* They could in theory make interest rates negative but then people would just hoard cash instead of investing it. (You’d get a better return by keeping cash under your mattress than lending it out.)

** Although a devaluation in the pound sounds bad it would actually boost the economy. When the pound is weak then foreign goods and services become more expensive. Also our goods and services become cheaper for foreign investors. This means more money being spent on UK goods and services, both by us and our friends overseas.

*** I brushed over the reason for this because it would have doubled the size of the already too big blogpost. If you’re interested in why this is the case read this.

")

")

")

")

")

")