Killing the Confidence Fairy

20/11/2013 1 Comment

Long-term readers might recall a blog post I wrote a while ago that explained why the UK government could borrow money at such low rates while the economy was weak. The government’s explanation was that their austerity policies had given markets “confidence” in the UK economy. So high was the confidence their policies had created, we were told, that we were now able to borrow money at the lowest rates in history, despite an ongoing economic depression.

If that smells a little fishy, it’s because it was. As I explained in that post, our low borrowing costs were a result of the market expecting short-term interest rates to remain low because they expected the economy to remain weak. Only when the economy started to recover would we see UK borrowing costs going up.

The government’s confidence argument was tested earlier this year when the UK lost its AAA credit rating, (the maintaining of which was one of the government’s key economic pledges.) If the government was right and confidence in the economy meant lower interest rates then this would, as they had repeatedly warned us, lead to a big increase in our cost of borrowing. I predicted the opposite would occur.

And what actually happened? Yes, the cost of borrowing went down after we were downgraded.

You might think that, after that, the government would have admitted that their faith in the Confidence Fairy had been misplaced. Well you might, if you were unfamiliar with our government.

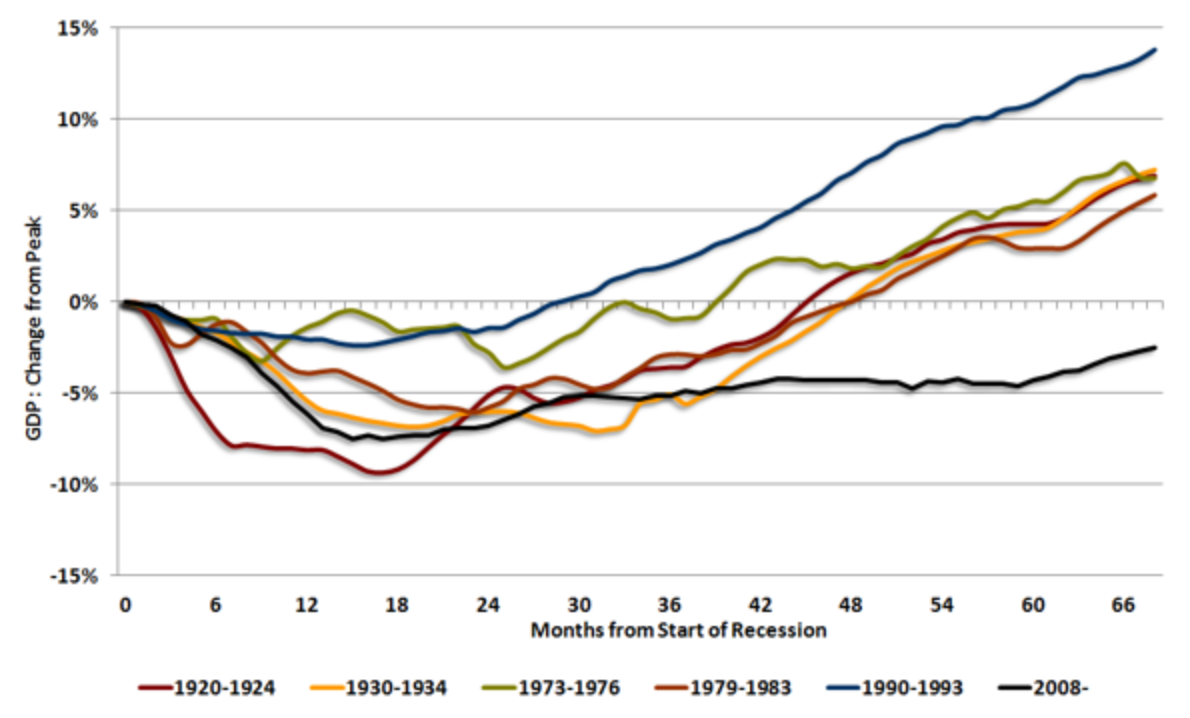

Moving on, over the past two quarters we have seen the start of an economic recovery. Yes, it has been the longest wait we have had to recover after any recession in our history but a recovery it is nonetheless. So what would the government’s explanation of borrowing costs driven by confidence predict? It would predict that as the economy recovers, confidence would increase even further and borrowing costs would go down.

And what would my explanation of borrowing costs driven by expectation of future short-term interest rates predict? As the economy recovers the expectation of higher future short-term interest rates would cause the government’s borrowing costs to go up.

Let’s see if we can spot any movement in the rates during the past six months that might help us work out who’s right. This from Bloomberg:

Yield on 10Y UK Gilts

If you favour the argument that low rates are all about confidence then explain to me why the cost of borrowing increased significantly during the period that the economy started to recover.

The confidence argument was, of course, nothing more than a means to an end – a manufactured tool to scare us into thinking that austerity during the bad times was a necessity. In a country like the UK, with control over its own currency, the confidence argument had no economic basis whatsoever and now we have the evidence to prove it.

The confidence argument was a lie. It really is that simple.

RedEaredRabbit