The Things We Used to Know

29/04/2013 1 Comment

Last weekend when discussing the Reinhart-Rogoff mess I wrote this:

We never needed “new cutting edge research” to solve this problem. The problem we have and the solutions to it are all covered in the first year of an undergrad economics degree.

On the following Tuesday (Economics Nobel Laureate) Paul Krugman, on the same subject, wrote this:

Econ 101 macroeconomics, as I often point out, has worked pretty well…The point is that radical new theories haven’t been needed at all; off-the-shelf economics, tools we already had, provided plenty of guidance.

He probably reads my blog.

So what are those things that first-year economics students know that should have stopped the depression happening? Before we look at those, let’s step back in history and remember how we got here:

The Financial Crisis

- Banks borrowed lots of money and then lent it out, a lot of it to risky borrowers

- Banks also encouraged individuals to build up debt through cheap loans and credit cards

- This not only led to a huge increase in private debt, it helped fuel a housing bubble in much of the developed world

- The banks had no plan-B if the housing bubble burst

- The housing bubble burst

- Oops

When people couldn’t make their debt repayments the banks suddenly became insolvent. Governments borrowed huge sums of money to bail them out and prevented a full collapse of the global banking system but were left with weak economies and high debt. Due to high levels of personal debt, rising unemployment and an all round lack of confidence in the economy, people switched very quickly from spending to paying off debt and saving. In the economy, my spending is your income and your spending is my income. Spending disappeared and a severe recession resulted.

Turning a Recession into a Depression

Governments initially responded by cutting interest rates. Low interest rates make saving less attractive and spending more attractive and in a normal recession this is enough to engineer a recovery. This was not an ordinary recession though and governments found that even with interest rates at almost zero, people continued to save and pay down debt rather than go back to spending. Low interest rates were not enough to fix the economy.

As any first-year economics student can tell you though, monetary policy is not the only tool a government has to boost growth. If the people don’t want to spend, the government can increase spending and fill the gap. Many governments, either through incompetence or the blind pursuit of their political ideals did the opposite and cut spending, which had the predictable effect of exacerbating the problem.

Governments likened their situation to that of an indebted household who must pay off their debt as fast as possible but the analogy, although easy for the public to understand, was disingenuous. In the economy spending and income are two sides of the same coin and in an economy suffering from a lack of demand from the private sector, cutting government spending was only ever going to lead to one thing.

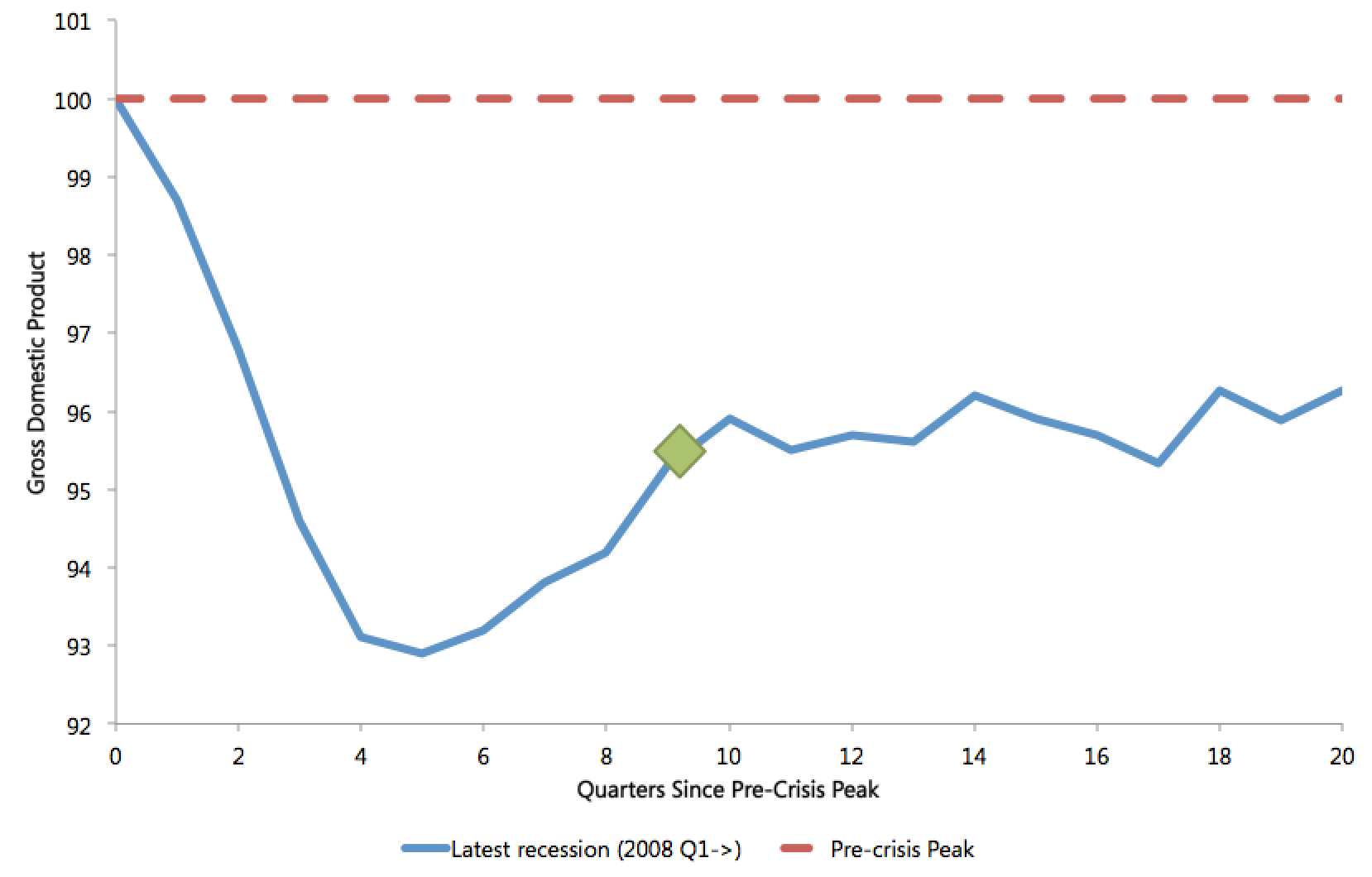

A recession, which we had all of the knowledge and tools to turn into a recovery, turned instead into a depression. Here’s what happened in the UK when the current government took over and slashed public spending. The green diamond shows the point when they were elected:

UK Depression

The amazing thing is that this is all basic, textbook macroeconomics. It is hard to comprehend how the government could try the opposite of what this stuff said they should do and then, when the economy entered depression, just sit around scratching their heads wondering why things didn’t work out.

But anyway – the damage is done now and the government would commit political suicide if they ever admitted that their policies, far from creating a recovery, had in fact caused a wholly unnecessary economic depression. From the day they chose austerity in the face of basic economics, they have had only one way forward: Wait until the economy sorts itself out anyway and then market this as absolution. I’ve come to terms with that now but I really hope we could all at least agree on this:

In 20, 30, or 40 years time when then next big recession happens, could we all take a look back on this period in history when our politicians, with their poo-pooing of basic economics, failed us so badly? Could we all take a look back on this period in history and say that we will never again make mistakes such as these? Let’s instead choose those basic economic rules that have, during this depression, continually got things right.

Let’s remember the things we used to know.

RedEaredRabbit

You could also include the years of declining wages for most, the impact of which was masked by the cheap lending on offer, and the hangover if it which will kill recovery stone dead.