The Austerity Fallacy

06/01/2013 12 Comments

If you’ve been on a long-haul aeroplane ride in recent years you will no doubt be familiar with the fantastic invention of noise-cancelling headphones. Noise-cancelling headphones use a microphone to measure background noise and then cancel it out by transmitting the “opposite” noise through the headphones.

I use the word “opposite” a bit clumsily here. I don’t mean that if there is a “woof” in the background then the headphones transmit a “meow”. I mean that if there is a sound wave that looks like this:

Background noise

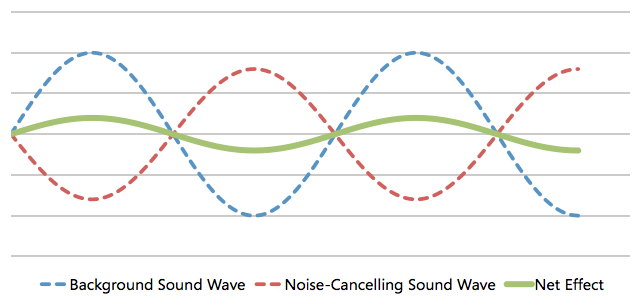

Then the noise-cancelling headphone produces a sound that looks like this:

Noise-cancelling effect

Note that the peaks of the background wave line up with the troughs of the noise-cancelling wave and vice versa, so when we add them together they offset one another. The noise-cancelling wave probably won’t be perfect and remove the sound completely but it will get rid of most of it resulting in a smaller version of the original background noise (the green line below):

Noise-cancelling wave

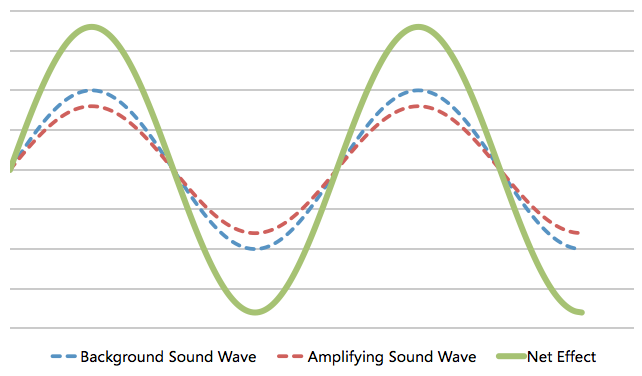

Essentially it works the opposite way round to a hearing aid. A hearing aid also has a microphone but instead of transmitting the “opposite” noise through the earpiece, it transmits the same noise – i.e. the peaks and troughs all line up. This time, rather than cancelling each other out, the waves combines to produce a bigger version of the original wave:

Amplifying Wave

Now you might wonder what all of this has to do with austerity. I’m coming to that but before I do let’s remember an important economic principal that I have mentioned many times before:

In the economy, my spending is your income and your spending is my income.

What I mean by this is that everyone’s income is a result of someone else spending money. If I buy a new pair of shoes then that gives income to the people who work in the shoe shop, people who work in the factory that produces the shoes, people who produce the raw materials such as leather, rubber, cotton, plastics etc that go to the factory, people who drive the lorries etc that deliver the raw materials to the factory, etc etc etc.

How did I get the money to buy the shoes? Someone else spent some money on the good or services that I help provide in my job. The point I am making here is that in the economy, spending and income are two sides of the same coin – you can’t have one without the other. Although this is the case, it is far easier to find a politician who says that we should all reduce our spending than it is to find a politician who says that we should all reduce our income. Politicians are a funny sort though. Anyway let’s talk about spending.

In the economy, at the highest level, we have two classes of spending – private spending and government spending. Private spending covers things like household spending, (such as the pair of shoes I bought) and the spending of companies. Government spending covers things like the NHS, state education, the armed forces, council budgets, roads – well, anything the government might want to spend money on.

The sum of private spending and government spending represent the total spending that is going on in the economy and therefore the total income. In order to maintain a healthy economy a healthy level of spending needs to be maintained but unfortunately the private sector is very unreliable in this respect.

The economy is sometimes good and sometimes not so good. When the economy is good the private sector wants to spend money – companies have lots of demand for their goods and services so they increase supply to meet the demand. This means employing more people opening new shops or offices or buying more raw materials from suppliers etc. When the economy is bad and demand for their goods and services is low they respond by reducing spending – making redundancies, closing shops, buying less raw material from suppliers etc.

So private spending over time might look a bit like this:

Private Spending

Those peaks are nice but those troughs are a problem. During those troughs, other things being equal, the economy as a whole is going to suffer from a lack of spending and a lack of income. Other things do not have to be equal though.

When the economy weakens, the government usually responds by cutting interest rates. This helps by making saving less attractive and borrowing and spending more attractive. More often than not this is enough to get the economy heading back in the right direction. In the case of the current financial crisis though it has not been enough to get things back on track. Interest rates were cut to near zero over three and a half years ago but the economy is still not recovering. Even with extremely low rates people would still rather save and pay down debt than borrow and spend.

So what are we left with? Remember that total spending is made up of private spending and government spending. We know that the private sector isn’t spending so we’re left with government spending. If the government keeps their own spending constant then overall spending will drop by the same amount that the private sector cuts spending. That doesn’t help.

The government could act as noise cancelling headphones though – increasing spending when private spending drops and cutting it when private spending rises. This might look like this:

Sensible Government Spending

You notice that when the government spends like this it helps to fill in the troughs and helps to stop overall spending (and therefore income) plunging by as much as it would if left to the private sector. (Note – we’re not asking the government to spend more overall – we’re asking the government to spend more when the private sector is not spending and less when the private sector is spending.) When interest rates can’t help then this is a very sensible fiscal policy – spending and income is to a large extend maintained.

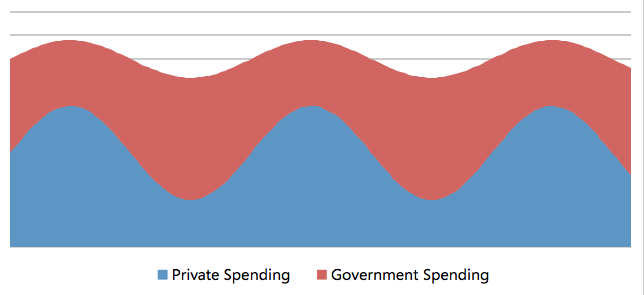

Let’s look for a moment though at the opposite fiscal policy – what would happen if the government chose to cut spending at the same time as the private sector? (Essentially fitting a hearing aid when noise-cancelling earphones were required.) Now the government actually amplifies the effect of the private sector downturn:

Daft Government Spending

Bizarre as it might seem, this was the choice of the UK coalition government. Rather than act to offset the spending cuts of the private sector they chose to amplify them and instead of smoothing over the cracks they have opened them up.

This is the Austerity Fallacy – the widely held belief that cutting government spending when private spending is depressed will create economic growth. But your spending is my income and my spending is your income. The government has intentionally engineered a situation where no one in the economy is spending which bizarrely they expected to create growth.

Just in case I get the usual arguments in the comments on this post, I’ll address them now in a pre-emptive strike:

But government spending is what got us into this mess in the first place!

No it isn’t, I already covered that.

But if we don’t slash spending then the rates at which the UK government can borrow will become unaffordable!

No they won’t, I already covered that too.

Damn you! But we can’t spend more than our income forever! (Ha! I have you this time!)

You have not read this post properly. I do not say the government should increase spending forever. When the private sector is weak and unemployment is high then there are lots of spare resources in the economy that increased government spending can utilise. When the private sector is strong then the government can reduce spending safe in the knowledge that there are plenty of jobs being created in the private sector for people to move to.

I am definitely not advocating high government spending when the private sector recovers – quite the opposite in fact. We have long-term problems in the shape of the government’s commitments to pensions. With an ageing population our pension liability is increasing far quicker than our motivation to address it. I agree that we need to get on top of these things but to decide to try to do it in the middle of a depression is frankly very stupid.

When the economy is not working our government has an immediate obligation to fix it. When it is fixed we can go about tackling the long-term things but attempting to tackle them when the economy is depressed is self-defeating – both in theory and (thanks to the government) we can now see, in practice.

The government’s policy of choosing to amplify the downturn is not just a mistake, it is entirely negligent and is not just causing unnecessary hardship and unemployment today, it is creating problems that will negatively affect the economy and the lives of many for years to come. Middle-aged people who have worked all their lives are now amongst the long-term unemployed, their savings spent and the prospects for the second half of their careers in tatters. University students are graduating into an economy that has no use for them. Rather than take the skilled jobs for which they have trained they are forced to choose whatever is available and this will affect their prospects and their incomes and their spending and everyone else’s incomes for their whole lives.

Whatever we do now, the effects of Cameron’s and Obsorne’s austerity experiment will be felt far into the future and the Chancellor’s new policy of further cuts to welfare in order to pay for the backfiring of this experiment is almost beyond belief.

Every model of the current depression says that we will eventually recover. Even with the current government’s policy of amplifying the downturn, all models suggest we’ll get back to a sustainable economy eventually. But why didn’t we do something that would have brought us to that conclusion two years ago? Or failing that why don’t we do it today?

The government won’t do it though because it would be political suicide to admit that they had got things so wrong. Too late for that – better to plough ahead and hope they can convince the public to swallow The Austerity Fallacy for another two and a half years.

RedEaredRabbit

*In the UK The Bank of England were made independent in 1997 so it is now they who set interest rates rather than the government. If only we could find someone to take over fiscal policy too…

")

")

")

")

")

")

")

")